Australian Accounting & Polish Cardiac Algos

A preview of two high-conviction micro-caps sitting at inflection points.

Good morning/afternoon/evening,

In recent weeks I’ve been sitting on two ideas I’ve grown increasingly convicted about as I’ve researched and watched and waited. Right now I have limited time to spend outside of my core obligations, so I’m unsure how long it will be until I can get satisfactorily organized/detailed/well-sourced writeups out on each of these. One of them, however, is moving rather quickly at the moment, with half-year earnings out in less than 24 hours, so I’d like to get a little preview of each thesis out for you to explore for yourselves if you wish. Happy to chat about either—you know where to find me.

This will read as a stream-of-consciousness essay rather than a polished research report. Please pour yourself a nice cup of coffee and enjoy this massive block of text with tastefully interspersed images.

Kelly Partners Group Holdings Limited (KPG.AX)

Market Cap: $200M (USD)

/ Posts / X")

Australian serial acquirer of SME (small-medium enterprise) accounting firms.

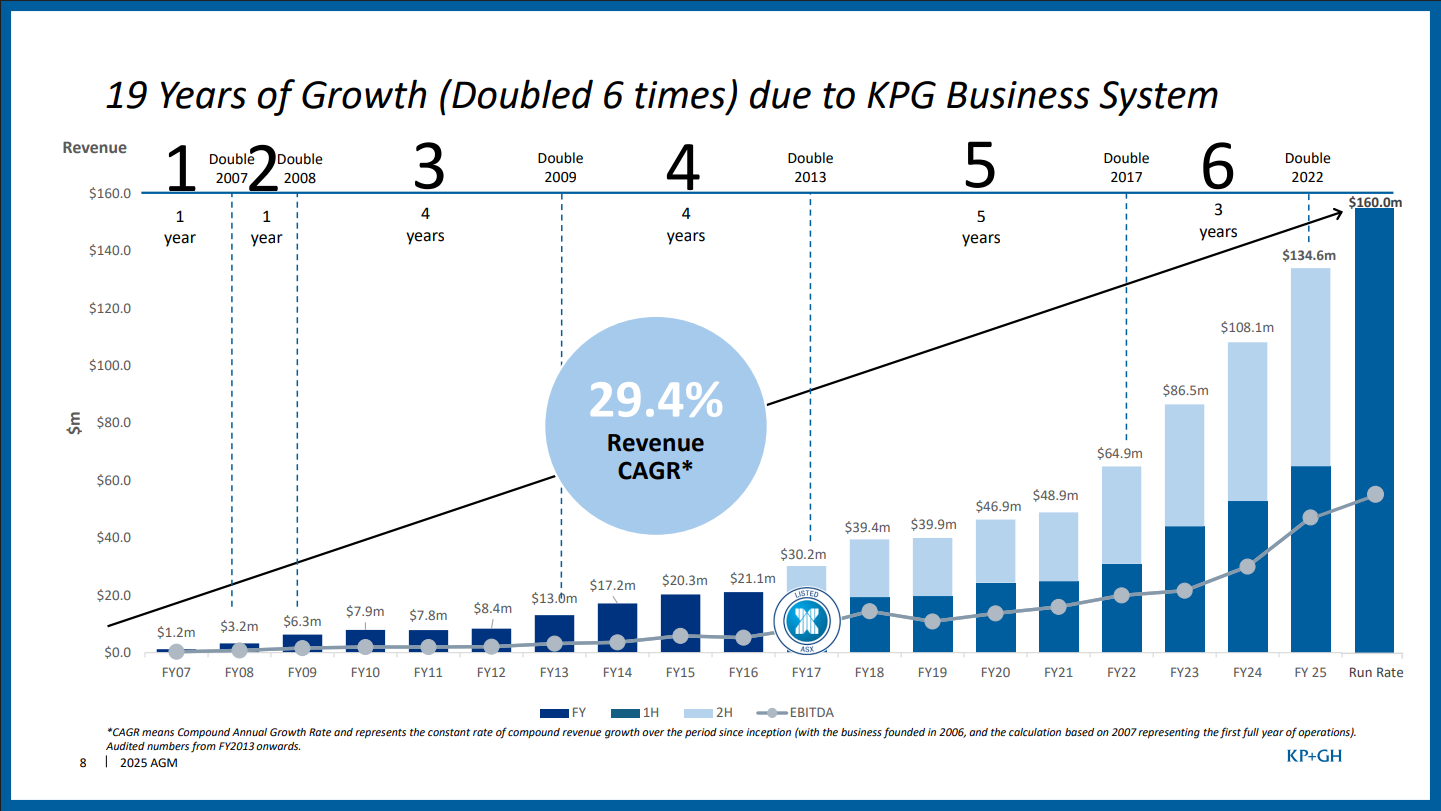

Track Record

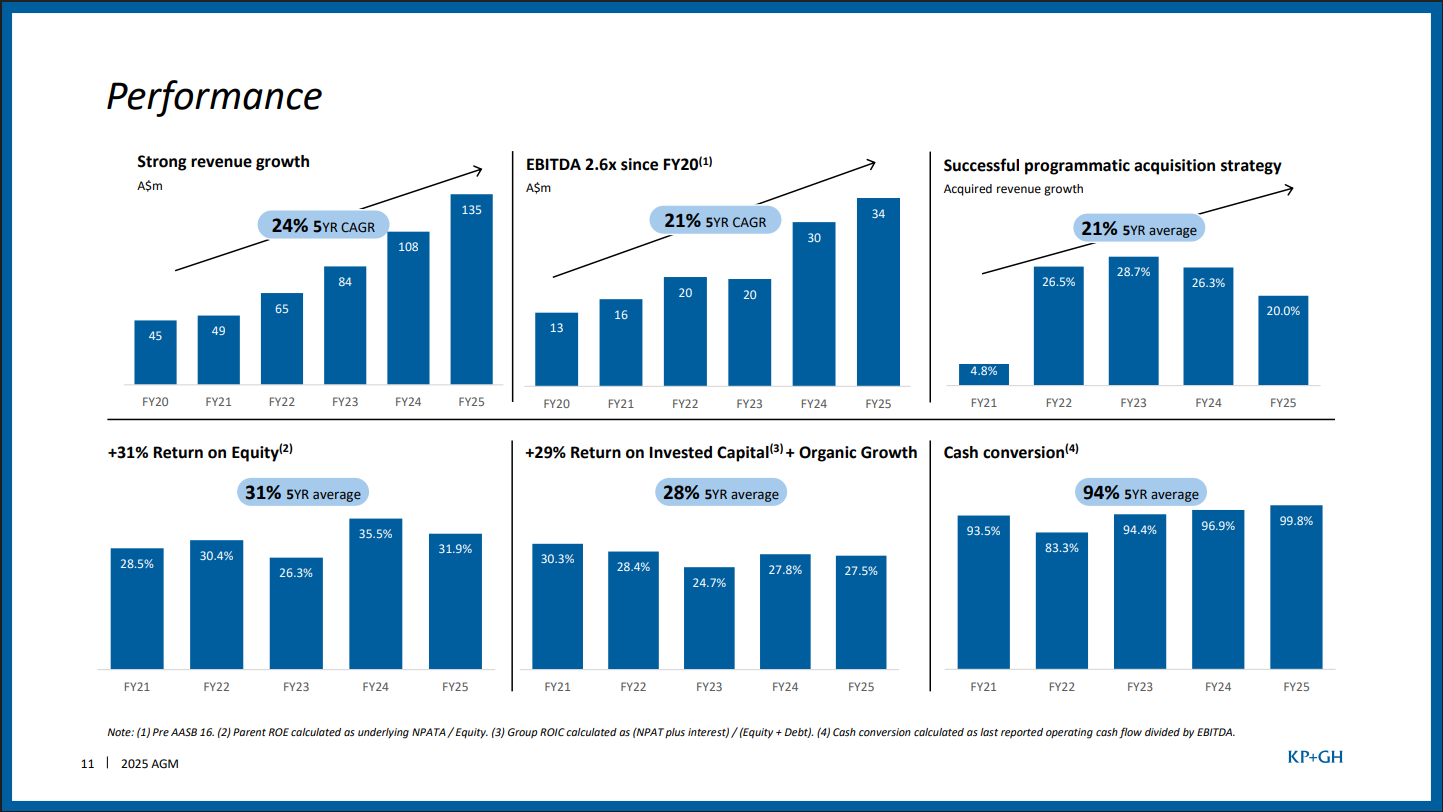

KPG has compounded book value per share at 35.45% annually since IPO (2017), consistent with its performance throughout its 20 years as an enterprise. The stock has compounded at 22% annualized as of writing, even after a >50% drawdown from highs one year ago (and at a much, much higher rate since the 2020 lows).

Business Model

Partner with (acquire 50.1% stakes in) SME accounting firms for 4-5x EBITDA, often when a partner is thinking about succession or wants to streamline operations. Use debt for the transaction, which goes on the target’s balance sheet. Deploy an excruciatingly detailed and standardized system for enhancing operational efficiency and transferring administrative burden to the parent company. Target 35% EBITDA margins post-improvement (generally acquired in the 25% ballpark).

These things are acquired at circa 3x post-improvement EBITDA, and then “trade at” the parent’s EBITDA multiple, which fluctuates but has tended to be around 12x EV-EBITDA. You can imagine how powerful that multiple arb flywheel is over time (hello Constellation and friends). The partners also tend to grow organically around 3-4% on top of the parent’s inorganic growth.

Inflection Point

While most of the growth so far has come from Australia, KPG is expanding internationally, with the primary target market being the United States, naturally. While this new phase of growth exposes the parent to some integration risk and a possible drop in capital efficiency (ROIC of 23% currently, down a few points vs historical), it also provides opportunities for larger deals and lengthens the growth runway before the law of large numbers starts to bite.

Recent Drawdown (Dislocation)

The stock has sold off more than 50% in the past twelve months, seemingly on AI fears (see CBZ for a comp, it’s not idiosyncratic) with possibly some additional encouragement coming from the serial acquirer “factor”. People have differing opinions on the impacts of AI here, which really makes or breaks the thesis, and none of us can know for sure.

My view is that a professional services firm like KPG that aggressively adopts artificial intelligence (as they are) will not be driven out of business by AI, but will instead see an ability to handle more clients per head and focus on higher-value client work over repetitive rules-based work and data management, and those well-executed productivity enhancements will compensate for industry headwinds. Some say Claude will nuke accountants, lawyers, etc., and I can see the argument, but I’m willing to bet against that view with an investment in a shareholder-minded operator tackling the AI challenge head-on who isn’t strictly reliant on organic growth.

It can also make more sense in a portfolio context where you’re long AI thematics or short something like an ADBE with a more plausible case for terminal impairment.

Key Man Risk/Opportunity

Founder & CEO Brett Kelly is a polarizing figure, undeniably. Personally, I appreciate his intensity and I think his track record of delivering value to shareholders speaks for itself. He is KPG and KPG is him, in a sense. This introduces risk, should he become unable to run the company for one reason or another, but this aggressive founder archetype is also one that can produce tremendous returns over long periods of time. You can read his letters and listen to his interviews for yourself and form an opinion, but I would encourage you to tease apart the operator and the philosopher, to the extent that’s possible.

I had the privilege of listening to him speak in-person not long ago, and I came away compelled by the operational philosophy, which is a major source of my conviction. Unfortunately, that’s not something I can give you here or that you can necessarily get from internet-mediated familiarity. To believe in the company you have to believe in Brett Kelly (and AI not making humans useless), but if you do, it’s not hard to envision replicable 20%+ annual returns long into the future. This one isn’t for everybody though. Some have called it a “cult stock”, but if it compounds it compounds, who am I to argue—it certainly doesn’t have a cult premium anymore today.

H1 2026 results later today.

Now for the really fun one, buckle up and have an AI read it to you or something:

Medicalgorithmics (MDG.WA)

Market Cap: $90M USD

Stock Price - Simply Wall St")

Developer of an AI-powered cardiac analytics platform.

Business History

For much of its history (since 2005), Medicalgorithmics has been a seller of PocketECG, a portable, non-invasive electrocardiogram (heart monitoring) device used for real-time monitoring/detection of arrhythmias, palpitations, fainting, and such. The business’s potential was limited by its nature as a hardware business and by exclusive distribution through React Health. Their U.S. subsidiary, Medi-Lynx, faced operational and financial shortfalls and the U.S. business eventually fell apart, requiring a restructuring. Medi-Lynx was sold to React in 2022 as MDG shifted from an exclusive distribution model to non-exclusivity. Now under new management, MDG is leveraging the fruits of their prior hardware business to transform the legacy business into a capital-light, high-margin AI solutions business.

Deus Ex-Machina

In 2022, Biofund Capital Management took a 49.99% stake in MDG in exchange for cash, a future financing commitment, and (this is the key) a transfer of 100% of the shares of Kardiolytics, Inc. to MDG. This was effectively a merger between MDG and Kardiolytics. Overnight, this turned the company from a struggling hardware business into a technical leader in cardiac diagnostics.

Since 2018, Kardiolytics has been developing DeepRhythmAI (DRAI), a set of machine learning algorithms for heart rhythm analysis which can be integrated into third-party software and devices. DRAI uses convolutional neural networks and transformer models to analyze ECG data. The beauty in this merger is how MDG brought its 250 billion heartbeats worth of proprietary data together with these AI algorithms, offering an unparalleled training set. The other asset Kardiolytics brought is called VCAST (Virtual Coronary Stress Test), a non-invasive automated analysis and virtual 3D reconstruction of the heart and blood flow, all based on CT images. For those of you familiar with the space, this may sound familiar—we’ll get to that.

Key Man Risk/Opportunity (Again)

Biofund Capital Management belongs to Dr. Kris Siemionow and Paweł Lewicki, also the co-founders of Kardiolytics. Dr. Siemionow is currently the President of the Management Board of MDG (CEO in effect), and Mr. Lewicki sits on the company’s supervisory board.

Dr. Siemionow (MD, PhD) is an orthopedic surgeon, professor, and serial entrepreneur with various well-cited peer-reviewed articles, patents, and relevant entrepreneurial experience to his name. His biographies aren’t hard to find, I’ll leave you to those. His mother, Maria Siemionow, has quite the resume as a famous facial transplant surgeon and chimeric cell researcher as well.

The other half of the Biofund pairing, Lewicki, served as a professor of cognitive psychology at the University of Tulsa from 1984 to 2009, where he established the Nonconscious Information Processing Laboratory. He left the university to run his predictive analytics software company, StatSoft, which was sold to Dell for an undisclosed amount in 2014. Put simply, he was a pioneer in human information processing and predictive data mining, although I think that undersells his accomplishments. You should read about him in more depth as well.

Basically, these two are titans in medtech and data analytics, and while I can’t vouch for their respective characters myself, my sense from each of their professional legacies is that they’re altruistically-oriented geniuses, basically. I’m sure there are many people in the medical and analytics communities who would be able to give you more color on them as people given how much they’ve done. You shouldn’t have the management issues here that you do in other small bio/pharma/medtech companies, if you know what I mean.

DeepRhythmAI

Back to the algorithms, DRAI received the FDA’s 510(k) clearance in 2022 under the QYX product code, with the most recent update receiving clearance in May 2025. It also has CE certification, permitting its sale in EU member states, and has been licensed by Health Canada as well. As of early 2026, they have global distribution through 3 major strategic partners (Bittium Biosignals, CardioScan, and Wellysis), along with various regional partnerships, including one of the top 5 American independent diagnostic testing facilities (IDTFs). So they have clearance and distribution.

On efficacy, the 510(k) clearance grants that the device (“device”) is as safe and effective as legally marketed equivalents, but that’s table stakes. Let me introduce you to the MARTINI study from Lund University, Sweden. Published in Nature in February 2025 (link), DRAI was put up against 167 certified independent ECG technicians in analyzing 14,606 individual ambulatory ECG recordings (avg 14-days long) which were then annotated by independent cardiologist panels. The study authors reported DRAI resulted in 17-times fewer missed diagnoses of critical arrhythmias than typical technician annotation, giving a negative predictive value exceeding 99.9%. Basically, it caught everything critical. This came at the cost of modestly higher false-positive findings, 2.4-times more. The study authors concluded DRAI analysis may substantially reduce labor costs and could potentially report results in near real time, improving access to care and improving outcomes for patients.

For the sake of transparency, it should be noted the study was led by Dr. Linda Johnson of Lund University, who also serves as Chief Scientific Officer for Medicalgorithmics.

VCAST

DRAI is Kardiolytics’ more established segment, while VCAST is the moonshot, so to speak. Designed to reconstruct and simulate a patient’s heart and blood flow in 3D from simple CT scans, VCAST assesses “the hemodynamic significance of coronary artery atherosclerotic stenosis.” It tells you how much a blockage is actually restricting blood flow by modeling the fluid dynamics. This non-invasive analysis (CT-FFR) helps to determine whether an invasive procedure is necessary. VCAST obtained CE certification (clearance in the EU) in October 2024 and the request for FDA 510(k) clearance has not yet been filed as of early 2026.

")

This market is already served by a company called HeartFlow (ticker: HTFL, IPO’d Aug 2025). HTFL is the market leader with approximately 30% share in CT-FFR. HTFL also models fluid dynamics like VCAST, but it requires a human-in-the-loop which lengthens the delivery time significantly (6-12 hours) and imposes a significant labor cost. HTFL is growing revenues 38% year-over-year, is valued at $2.5 billion as of writing, with full insurance coverage, and still continues to post significant net losses because of its costly R&D and operating model. VCAST is roughly as (slightly more) accurate as HTFL (HTFL: 86% sensitivity, 79% specificity; VCAST: 88% sensitivity, 80% specificity), while offering results at a much lower price point and in a fraction of the time at 1-2 hours. HTFL is the natural incumbent for VCAST to disrupt (and it’s worth $2.5B today, 28x MDG, which has other products and a leaner cost structure, just commercially nascent).

Keya Medical (Chinese) has a 15% share, but with an arguably more compelling case for efficacy, speed, and cost. It uses deep learning techniques for extremely high sensitivity to blockages, but that comes at the cost of interpretability creating a trust problem—a cardiologist can’t go through a 3D model and understand the physics that led the model to its output. I would guess that Medicalgorithmics could quite effectively train a deep learning model to compete directly here and integrate with VCAST’s physics, and they could well be doing that already behind the scenes, though I haven’t been able to find any indication.

Elucid holds 12% of the market and uses AI trained on actual tissue samples to identify plaque from CT scans.

Cleerly is another top performer which excels in plaque characterization, going beyond other providers by identifying “soft” plaques which indicate a higher risk of a cardiac event. In December 2025, MDG secured a 9.4 million PLN grant from the Polish Agency for Enterprise Development (PARP) for a VCAST-based project called Kardiobeat.CT, whose expressed purpose is to automate detection and assessment of atherosclerotic plaques. To me, this project appears to be a direct challenge to Cleerly’s offering.

I hope by now you’re starting to see this picture come together. With MDG, Dr. Siemionow and Mr. Lewicki are building a fully-automated integrated suite for cardiac diagnostics, leveraging MDG’s unique 250 billion annotated heartbeat dataset to propel Kardiolytics’ technologies forward. It’s beautiful really, hat off to you sirs.

TAM-Expansion via Preventative Diagnostics

If that picture in a $90 million package isn’t pretty enough for you, there’s more. VCAST is currently participating in a landmark study with Lund University again, called the SCAPIS study. The study took CCTA scans of 30,154 healthy adults, aged 50-64, in Sweden from 2013-2018 (along with some other diagnostics). In 2024-2026, 15,000 of those subjects are being re-examined. VCAST has been tasked with analyzing these results, where it will learn what a multi-year progression in atherosclerosis in the same subject looks like. What did a 2026 diseased heart look like back in 2016? If VCAST can successfully identify at-risk hearts before they show significant disease years later, that makes a very strong case for VCAST to be the gold standard in preventative cardiac imaging.

Now, imagine you’re an insurance company. SCAPIS 1 (2013-2018) found 42.1% of participants (all without known coronary heart disease) actually had atherosclerosis. 5.2% had significant stenosis (high-risk). And mind you, this is in Sweden, it’s worse elsewhere. So over 40% of your “healthy” insured population 50-64 has some atherosclerosis and over 5% is at high risk for a cardiac event and likely requires intervention.

If an AI diagnostics provider could offer you a fast, inexpensive, highly reliable, and interpretable assessment of cardiac health from a simple CT scan, why would you not apply those diagnostics to every CT scan of a patient’s chest if they fall within an at-risk demographic range? This makes huge economic and medical sense for both payer and patient regardless of whether the scan was done for a cardiac issue or something else entirely.

Stock Price and Recent Activity

The opportunity here is so large and so clear, you really don’t even need to go through napkin math, let alone a full valuation, so I won’t here. But, I will go through some recent developments for the company which are material, yet that have left the stock price relatively unchanged. In my view, shareholders are asleep at the wheel on this one and there’s a case for undervaluation on the margin, even ignoring the extent of the market opportunity (which I think is also grossly underappreciated at $90 million).

At 31.80 PLN, the stock is exactly flat since July 15, 2025. Let’s see what’s happened since. I’m going to list them out to make a point:

July 18 - PARP awards PLN 9.4 million in grant funding.

July 29 - MDG signs its first commercial agreement for VCAST (Scandinavia).

August 1 - July revenue grew 33% YoY with the integration process for 4 of its 14 clients acquired in 2025 to-date.

“We are clearly gaining momentum, entering what we view as a more dynamic and sustainable growth trajectory. We are leveraging strong market demand for our unique solutions and have significantly improved our client onboarding efficiency, which has directly translated into revenue growth. Importantly, this growth is primarily driven by recurring revenues from newly signed contracts. This not only validates our strategic focus on scaling sales of our world-class AI software, but also highlights the long-term growth potential of Medicalgorithmics in the coming months,” commented Dr. Kris Siemionow, CEO of Medicalgorithmics.

August 4 - Upward MRR Estimate Revision: New ECG service contracts, excluding the new U.S. IDTF client, will generate US$160.2K of MRR.

August 7 - Second commercial agreement for VCAST signed (Turkey).

August 13 - North American deep-tech company signs agreement to use MDG software with a minimum annual revenue of PLN 382.8K.

September 1 - Biofund sells a 15% stake (non-dilutive) to several prominent Polish investment entities (I read this as neutral-bullish, with the VC fund taking some profits on their successful turnaround and broadening the institutional shareholder base without diluting existing shareholders).

September 17 - DRAI partnership with Swedish arrhythmia diagnostics and stroke prevention firm, carrying revenue minimums.

September 24 - One of the largest U.S. IDTFs increases the daily number of ECG studies analyzed by MDG by 118%.

October 6 - Q3 2025 Revenues: PLN 7.2 million, +38% YoY, +76% in the U.S.

October 20 - MDG signs a VCAST agreement with one of Saudi Arabia’s leading healthcare companies, including contractual minimums.

November 3 - MDG signs a contract worth at least PLN 439.2K per year for ECG diagnostics with the U.K.’s largest ITDF.

November 4 - MDG partners with Lund University for a landmark study (SCAPIS 2, discussed above).

November 10 - New MARTINI study findings: Results show a 75 to 114-fold reduction in the risk of missing clinically meaningful diagnoses, presented at the American Heart Association’s 2026 meeting.

December 1 - MDG expands cooperation with its largest client, one of the U.S.’s largest IDTFs, increasing remuneration by over 50% in December, to US$450K-500K.

December 2 - MDG signs new contract worth at least US$5.9 million with second largest customer.

December 18 - PARP grant of PLN 9.4 million for Kardiobeat.CT (discussed above).

January 5 - Agreement signed with another American IDTF.

January 7 - MDG ends the year with record 74% revenue growth and positive EBITDA in Q4 2025 (huge).

January 19 - MDG enters South America with an agreement signed with leading Peruvian distributor, Sharp Tech.

January 20 - Further broadening the institutional shareholder base, Biofund sells (non-dilutive) PLN 70 million worth of shares to leading Polish pension funds, investment managers, and family foundations, in response to high investor demand following Q4 results.

January 22 - Biofund submits a binding offer to the Company, including a waiving of the 3% commission on revenues from new customers, a reduction of the 2024 loan’s interest rate from 18.5% to 14%, a 6-month extension of repayment maturity dates, and a 12-month lock-up on all remaining shares held by Biofund. Also, the Fund declared a readiness to negotiate the conversion of the US$3 million loan into shares.

I see this as a signal of strong commitment to MDG’s future. They didn’t have to do any of this, and it’s at Biofund’s immediate expense, for the longer-term benefit of MDG. A further point: This commission forgiveness and loan conversion improves the company’s cash flow position markedly, and you guessed it, the stock is down a few hundred bps since then.

January 27 - The largest financial institution in Central and Eastern Europe, Nationale-Nederlanden PTE, discloses it took an 8.3% position in the recent transaction with Biofund.

So yes, all of that news and the stock hasn’t budged. Was it all priced in? I don’t think a reasonable person can make that argument.

To sum up, MDG.WA is trading at US$90 million with a loss-making competitor selling an inferior product valued at $2.5 billion, and it’s building an integrated platform with substantial IP and data moats. This company is doing to ECG technicians what the market is afraid AI is doing to accountants.

The final regulatory hurdle is VCAST’s FDA 510(k) clearance. I would speculate the SCAPIS 2 study will be a major datapoint for the submission, and when that data is released (prelim results in March, data-sharing in September), that data package along with the latest version of VCAST, would go to the FDA for its evaluation of substantial equivalence (to HTFL primarily). You never know, but I have a hard time imagining how the updated version doesn’t at least perform as well as the prior version, which was slightly better than HTFL, and they already have CE certification for the EU. As an outsider, I see no reason substantial equivalence isn’t an obvious conclusion.

This lean little $90M AI-medtech company hiding in Poland run by a couple of, dare I say, shareholder-oriented geniuses has a chance to dominate a cardiovascular diagnostics market worth tens of billions, and the speed of the rollout is limited only by the speed at which they’re able to onboard new clients. The operating leverage here is obscene. I can’t wait to see how this plays out over the next several years.

If you happen to be a cardiologist or convolutional neural net expert, please feel free to let me know where I’m wrong if you believe I am.

Thank you for reading. Godspeed.

Showing lines revenue declines past few years?